MBA Advocacy

MBA has long been recognized as the leading advocate on banking issues among members, media, policymakers and the public. Our ongoing mission is to foster safe, profitable and successful banks, which in turn promote strong communities and a strong Missouri economy.

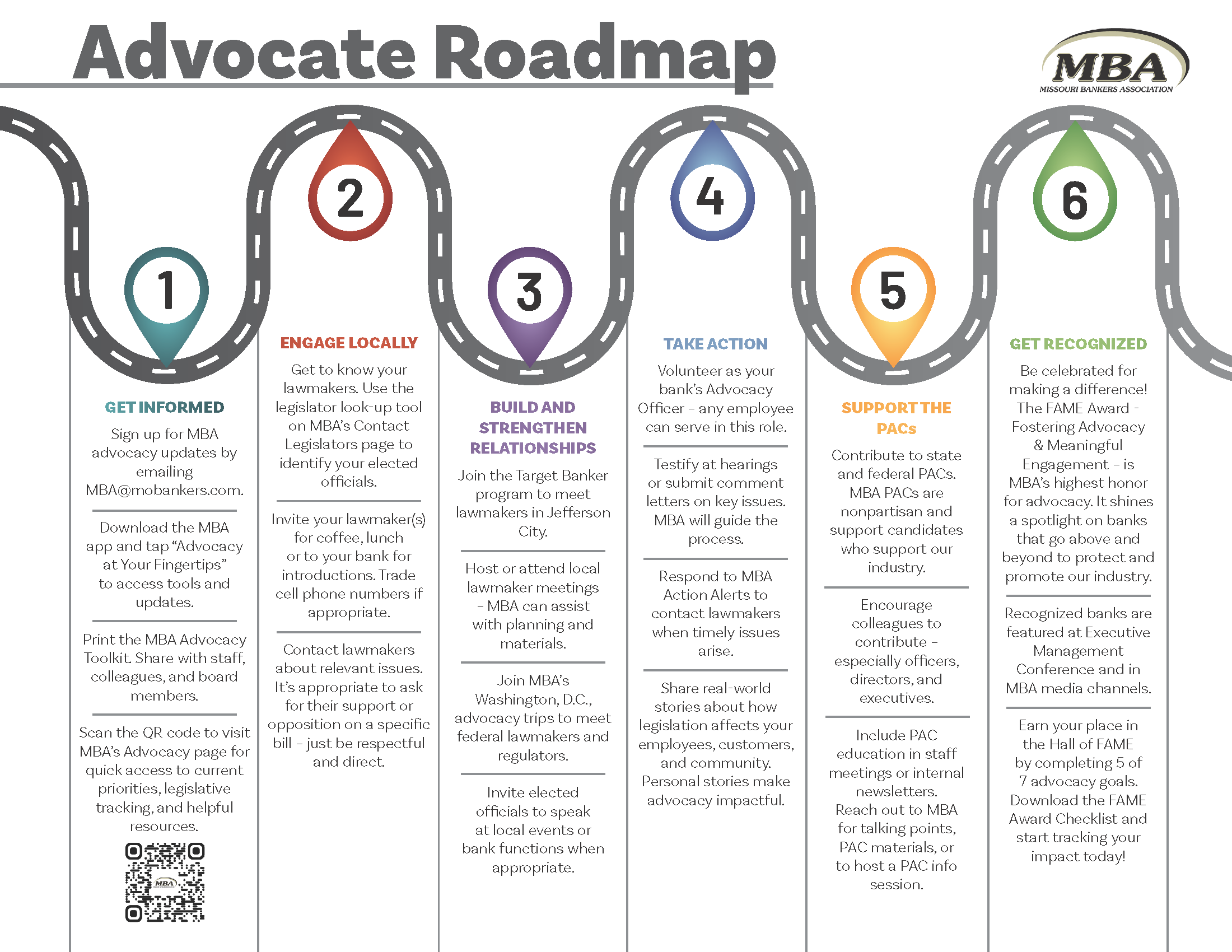

To support that mission, our goal is to make every MBA member an advocate. Bankers in any role in every department can participate in banking advocacy. Use the Advocate Roadmap to help you get started or build on past experience. We encourage you to use resources on this site and in the advocacy section of our mobile app and share them with colleagues.

Contact David Kent or Emily Lewis at MBA for more information.